Last Reviewed 9/27/25

by Scott

Best Investment Portfolio Strategies in Your 50s

Mix Tape Your Money Moves!

This website contains affiliate links, meaning we may earn a commission for purchases made through these links, at no extra cost to you. Our opinions are principled, original and our own. See how we make money. Thank you for your support.

If you’re over 50 and late starting to save for retirement, don’t worry—you can still build a solid financial future with portfolio strategies over 50. These tailored portfolio strategies over 50 offer proven, efficient ways to grow wealth despite a shorter timeline. From Dave Ramsey’s growth-focused mutual fund approach to passive index investing and income-generating portfolios, diverse portfolio strategies over 50 provide practical solutions. Whether you’re new to investing or looking to supercharge your savings, these approaches deliver actionable steps to help you catch up and retire with confidence, Mixtape style.

9 Portfolio Strategies for Late Starters Over 50

From aggressive to ultra conservative, these 8 portfolio strategies offer something for every late starter. These are listed in no particular order.

Dave Ramsey’s 25/25/25/25 Strategy

Philosophy:

Advocates 100% stock mutual funds, split across growth, growth and income, aggressive growth, and international funds for diversification within equities, focusing on long-term growth, avoiding bonds.

Portfolio Example:

- 25% Growth Stock Mutual Fund (e.g., Fidelity Growth Company, FDGRX)

- 25% Growth and Income Fund (e.g., Vanguard Dividend Growth, VDIGX)

- 25% Aggressive Growth Fund (e.g., T. Rowe Price Small-Cap Stock, OTCFX)

- 25% International Fund (e.g., American Funds EuroPacific Growth, AEPGX)

PROS:

CONS:

HOW TO IMPLEMENT:

To choose this investment portfolio strategy for later starters select actively managed mutual funds with 10+ year track records. Allocate 25% to each of 4 categories: growth stocks, growth and income stocks, aggressive growth stocks, and international. Use platforms like Fidelity or work with an advisor. Automate contributions and hold long-term. See our list of best full service investing platforms.

The Boglehead Strategy (Passive Index Investing)

Philosophy:

Uses low-cost, diversified index funds to track market performance with minimal effort.

Portfolio Example:

- 60% Total Stock Market Index Fund (e.g., Vanguard VTI)

- 30% Total Bond Market Index Fund (e.g., Vanguard BND)

- 10% Total International Stock Index Fund (e.g., Vanguard VXUS)

PROS:

CONS:

HOW TO IMPLEMENT

Open a brokerage account (e.g., Vanguard, Schwab), invest in low-cost ETFs/mutual funds, automate contributions, rebalance annually. See our list of best full service investing platforms.

Budget Coach USA Strategy (Passive Index – All Equities)

Philosophy:

Combines low-cost Bogglehead index funds with Ramsey’s 25/25/25/25 diversification. Remains in all equities for maximum growth potential.

Portfolio Example (Fidelity Funds):

- 25% FLCOX Large Cap Value

- 25% FSPGX Large Cap Growth

- 5% FSMAX + 5% FECGX + 15% FMDGX (Equal 25% of Small & Mid Cap Growth Funds)

- 25% FSPSX International Large Cap Blend

PROS:

CONS:

HOW TO IMPLEMENT

Open a brokerage account (e.g., Fidelity Vanguard, Schwab), invest in low-cost index funds, rebalance annually. Allocate 25% to each of 4 categories: growth stocks, growth and income stocks, aggressive growth stocks, and international. See our list of best full service investing platforms.

The Dividend Growth Strategy

Philosophy:

Focus on stocks/funds with consistent dividend growth for income and reinvestment to compound wealth.

Portfolio Example:

- 50% Dividend ETF (e.g., Vanguard Dividend Appreciation ETF, VIG)

- 30% Total Stock Market ETF

- 20% Bond ETF (e.g., iShares AGG)

PROS:

CONS:

HOW TO IMPLEMENT

Select ETFs or blue-chip stocks with 10+ years of dividend growth (e.g., Coca-Cola, Procter & Gamble). Use a DRIP for compounding.

The 60/40 Classic Balanced Strategy

Philosophy:

Splits investments between stocks (growth) and bonds (stability) for balanced risk/return.

Portfolio Example:

- 60% Total Stock Market ETF (e.g., Schwab SCHB)

- 40% Total Bond Market ETF (e.g., iShares AGG)

PROS:

Simple, reduces volatility, reliable long-term returns.

CONS:

Lower growth than stock-heavy portfolios, bond yields may lag in low-interest environments.

HOW TO IMPLEMENT

Use a robo-advisor (e.g., Betterment) or manually invest in broad-market ETFs. Rebalance periodically.

Ray Dalio’s All-Weather Portfolio

Philosophy:

Diversifies across asset classes to perform in all economic conditions (inflation, deflation, growth, recession).

Portfolio Example:

- 30% Stocks (e.g., Vanguard VTI)

- 40% Long-Term Treasury Bonds (e.g., Vanguard VGLT)

- 15% Intermediate-Term Bonds (e.g., Vanguard BND)

- 7.5% Gold ETF (e.g., SPDR Gold Shares, GLD)

- 7.5% Commodities ETF (e.g., Invesco DB Commodity, DBC)

PROS:

CONS:

HOW TO IMPLEMENT

Use ETFs for each asset class, rebalance quarterly, consider robo-advisors for automation.

The Barbell Strategy

Philosophy:

Combines high-risk, high-reward investments with ultra-safe assets, avoiding moderate-risk options.

Portfolio Example:

- 80% Safe Assets (e.g., Treasury Bills, iShares TIPS Bond ETF, TIP)

- 20% High-Growth Assets (e.g., small-cap ETF like Vanguard VB or tech ETF like QQQ

PROS:

Balances safety with high growth potential, protects principal.

CONS:

High-growth assets are volatile, requires careful monitoring.

HOW TO IMPLEMENT

Allocate most funds to low-risk securities, invest in small-cap/sector ETFs for growth, rebalance regularly. See our list of best full service investing platforms.

The Core-Satellite Strategy

Philosophy:

Combines a stable “core” (broad-market funds) with “satellites” (specialized investments) for diversification and alpha.

Portfolio Example:

- Core (70%): Total Stock Market ETF (60%) + Total Bond Market ETF (10%)

- Satellites (30%): REIT ETF (10%), International ETF (10%), Sector ETF (e.g., healthcare, 10%)

PROS:

CONS:

HOW TO IMPLEMENT

Build core with index funds, select satellites based on trends/expertise (e.g., real estate).

The Income-Focused Strategy

Philosophy:

Prioritizes steady income through dividends, interest, or distributions for reinvestment or withdrawals.

Portfolio Example:

- 40% Dividend ETFs (e.g., Schwab US Dividend Equity, SCHD)

- 30% Bond ETFs (e.g., Vanguard BND)

- 20% REIT ETFs (e.g., Vanguard VNQ)

- 10% Cash or Treasury Bills

PROS:

CONS:

HOW TO IMPLEMENT

To implement this investment portfolio strategy for late starters, focus on high-quality dividend/bond ETFs, maintain a cash buffer.

Comparing Portfolio Strategies for Late Starters Over 40

| Portfolio Strategy | Risk (1-5) | Complexity (1-5) | Best For | Key Benefit |

|---|---|---|---|---|

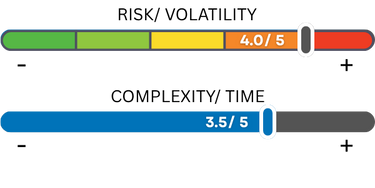

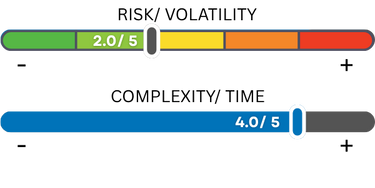

| Ramsey 25/25/25/25 All Equities | 4.0 | 3.5 | Growth Seekers, Active Investors | High growth potential through global equity diversification |

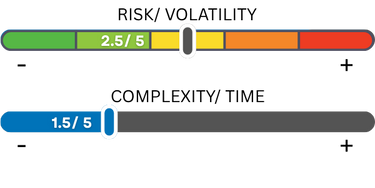

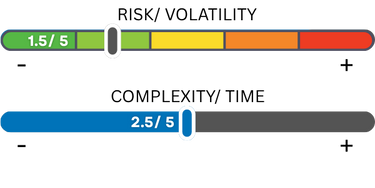

| Boglehead Passive Index (60/30/10) | 2.5 | 1.5 | Beginners, Risk Averse | Simple, low-cost diversification with balanced risk |

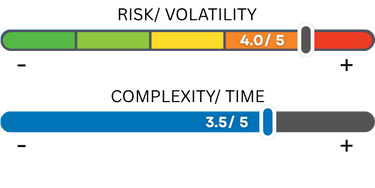

| Budget Coach USA Stragety | 4.0 | 3.0 | Growth Seekers | Low cost index funds, growth potential |

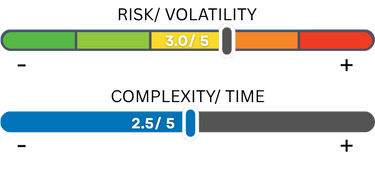

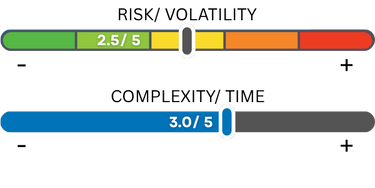

| Dividend Growth (50/30/20) | 3.0 | 2.5 | Growth Seekers, Risk Averse | Steady income with moderate growth |

| 60/40 Classic Balanced | 2.5 | 1.5 | Beginners, Risk Averse | Time-tested balance of growth and safety |

| Ray Dalio’s All Weather | 2.0 | 4.0 | Risk Averse, Active Investors | Stability across economic cycles |

| Barbell (80/20) | 1.5 | 2.5 | Risk Averse, Growth Seekers | Capital preservation with growth upside |

| Core-Satellite (70/30) | 3.5 | 3.5 | Growth Seekers, Active Investors | Broad market exposure with targeted growth |

| Income-Focused (40/30/20/10) | 2.5 | 3.0 | Risk Averse, Active Investors | Reliable income with diversified sources |

Portfolio Fund Types Compared

| Investment Type | Description | Trading | Management Style | Expense Ratios | Liquidity | Minimum Investment | Tax Considerations | Risk Level |

|---|---|---|---|---|---|---|---|---|

| ETFs | Exchange-Traded Funds: Baskets of securities (stocks, bonds, etc.) that trade like stocks on exchanges. | Intraday during market hours. | Mostly passive (index-tracking); some active. | Low (0.03%-0.50%). | High; can be bought/sold anytime market is open. | Typically 1 share price. | Generally tax-efficient due to in-kind redemptions minimizing capital gains. | Varies by underlying assets (moderate for broad market). |

| REITs | Real Estate Investment Trusts: Companies that own, operate, or finance income-generating real estate; must distribute 90% of income as dividends. | Intraday (as individual stocks). | N/A (company stocks). | N/A (but dividends taxed as ordinary income). | High for publicly traded REITs. | 1 share price. | Dividends taxed as ordinary income; no corporate tax at REIT level if compliant. | Moderate to high; sensitive to interest rates and real estate market. |

| Index Funds | Mutual funds that aim to replicate the performance of a specific market index (e.g., S&P 500). | End-of-day NAV. | Passive. | Very low (0.04%-0.20%). | Moderate; redeemable daily at NAV. | Often $1,000-$3,000. | Less tax-efficient; potential for capital gains distributions. | Low to moderate; tracks market volatility. |

| Bonds | Debt securities issued by governments, corporations, or municipalities, paying periodic interest. | Intraday (individual bonds); or via funds/ETFs. | N/A (fixed income instruments). | N/A (but bond funds have fees). | Varies; high for Treasuries, lower for corporates. | Face value (e.g., $1,000). | Interest taxed as ordinary income; some municipal bonds tax-exempt. | Low to moderate; interest rate and credit risk. |

| Mutual Funds | Pooled investment vehicles that invest in a diversified portfolio of stocks, bonds, or other securities. | End-of-day NAV. | Mostly active; some passive (index). | Higher (0.50%-1.50%+). | Moderate; redeemable daily at NAV. | Often $1,000-$3,000. | Less tax-efficient; frequent trading can trigger capital gains. | Varies by holdings (moderate for balanced funds). |

Choosing a Portfolio Strategy Over 50

Keep it Simple

- When in doubt, keep it simple. Great growth comes from simple index and mutual fund investing.

- Want a smoother ride? Add bonds, sacrificing some growth.

- Want growth with a wilder ride? Use all equities like the Ramsey Plan or Budget Coach USA strategy.

Select Low-Cost Platforms

- Brokers like Vanguard, Fidelity, or Schwab for low-fee ETFs, index funds or mutual funds.

- Use low fee funds with at least a 5 year history.

Automate and Rebalance

- Set up automatic contributions for consistency. Put your contributions on autopilot.

- Re balance annually or when allocations drift (e.g., 5% deviation), except Ramsey’s strategy, which requires less frequent rebalancing due to equal splits.

Getting Started Today

Starting to save after age 50 is crucial, especially when you’re leveraging portfolio strategies over 50 to max out your returns in a shorter time frame. With less time to ride the compound interest wave every dollar you invest today can grow faster than a Rubik’s Cube craze through smart, consistent contributions to a diversified portfolio. Delaying is a buzzkill, as it cranks up the monthly savings needed to hit your retirement goals. By prioritizing portfolio strategies over 50, like maxing out your 401(k), tapping into catch-up contributions for those over 50, or investing in a Roth IRA you can optimize your financial future.