Debt affects millions of individuals and families. In fact, debt is so pervasive in American life it is hard to find anyone without it. Whether it be student loans, credit card debt, or car loans, the burden of owing money has far-reaching consequences on personal finances. Understanding these basic facts about debt and the motivation of those who offer it is crucial to building a healthy financial future. In this article, we will delve into some eye-opening facts about debt and some of the myths that surround it. We also offer some resources and a path out of debt and to the road of financial independence. Let’s dig in.

3 Facts About Debt Everyone Needs to Know

Here are our top 3 facts about debt that everyone should know about debt. Buckle up.

Fact 1. Debt is a financial product for the enrichment of others, not you.

Debt is a financial product that enriches the (lender) bank, not you. Your bank is not like your local library. They won’t let you borrow for free and bring it back whenever you feel like it. Your bank exists to make money and their primary product is debt. Their goal is to sell you as much debt as they can, for as long as they can. And it all comes at your expense.

Your bank is not a nonprofit organization that provides services to underprivileged populations. They are not a civic-minded club offering help to the community without expecting anything in return. Your bank is a for-profit entity that seeks to leverage your need for money to its benefit.

Banks loan you money and require you to pay back the loan with interest. Math says that when you are done paying back the loan, you have less money than when you started. Ignore math if you want, but you’ll spend your life playing catch up if you play ball with bank loans. And you can’t build a stable financial future playing catch up.

Fact 1: Debt is a financial product for the enrichment of others, not you.

Fact 2. Debt is not a wealth-building tool (for you).

Debt is not a wealth-building tool for you. It is however a wealth-building tool for the bank…at your expense. And they depend on this arrangement to make money. The math is clear. Borrow money from a bank and when you are done paying it back, you’ll have less money than when you started. The more money you borrow, the less money you have in the end.

If you borrow $10,000 for a car. Over the next 4 years, you will pay back the original $10,000 plus $1,000 in interest. When you took the bank loan, you had $10,000. When you finished paying the bank loan off you paid a total of $11,000. So after 4 years, you had lost $1,000.

Fact 2: Debt is not a wealth-building tool for you. It is however a wealth-building tool for the bank. Your biggest wealth-building too is your income, governed by a zero-based budget.

Fact 3. Debt is not an inevitable reality.

Life presents a lot of challenges. Some of us are born into families with means and others are born into families in poverty. And there are people on all spectrums in between. But one thing we all share in common as we become adults is the ability to make our own choices to improve our future. Yes, some have much larger, more difficult mountains to climb. For some, the journey to financial independence is a much steeper slope. But it is possible.

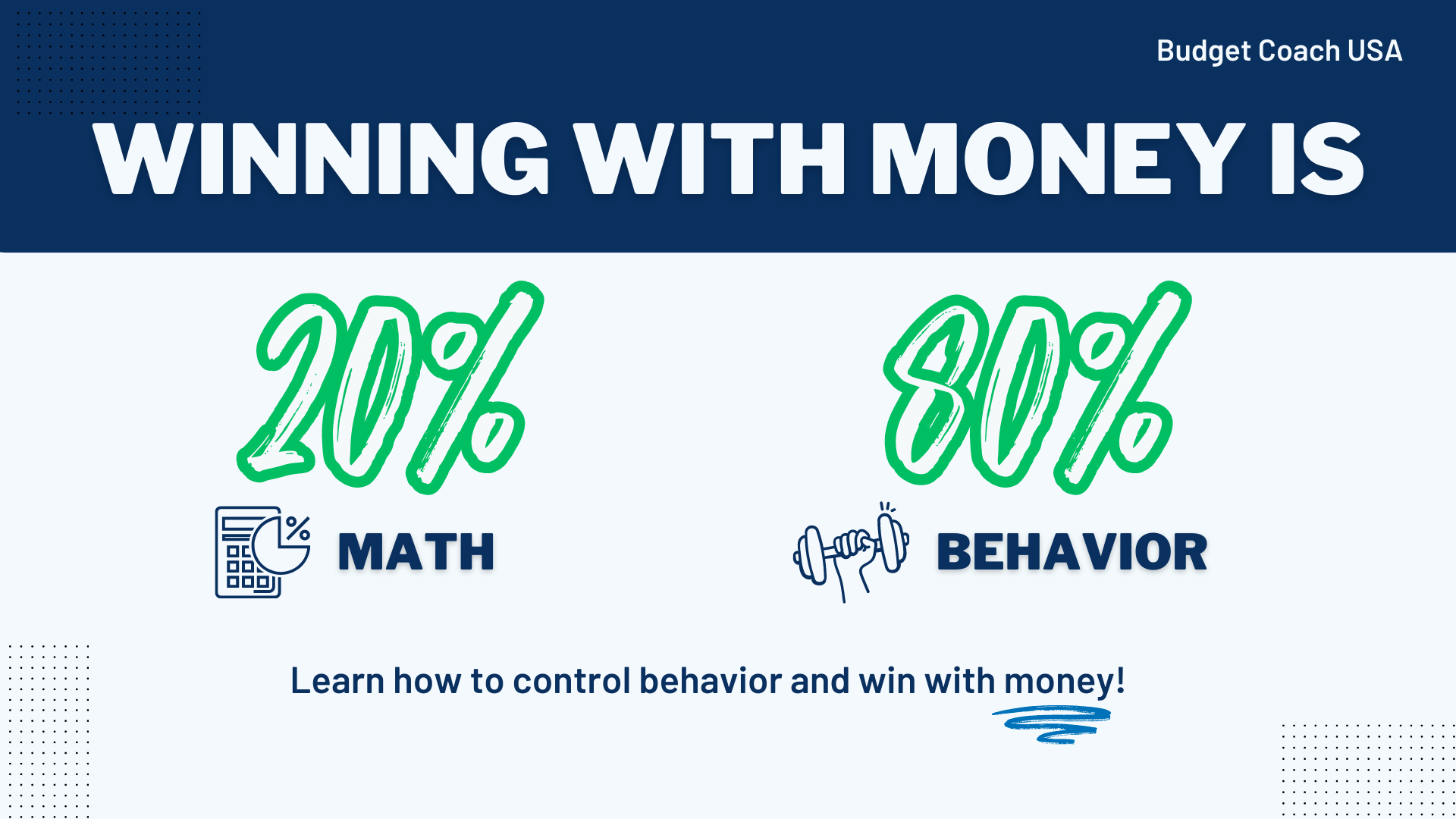

History is replete with examples of individuals who gained astonishing sums of money and squandered it all way. (Think lottery winners for example) History is also full of examples of those who started with nothing and rose to great wealth. The issue with eliminating debt from your financial life has little to do with where we start. It has more to do with how we handle money when we get it. Personal finance is twenty percent math and eighty percent behavior. Put another way; winning with money is 20 percent math and 80 percent behavior.

Fact 3: Debt is not an inevitable reality.

4 Myths About Debt

As pointed out above. debt is a financial product for the enrichment of others, not you. So what are some of the myths that are perpetuated to sell their product? We’ve highlighted a few of the most common for the reader here.

Myth 1. You can’t buy a car without debt.

Lenders love to sell you on the idea that you can’t buy a car without debt. And since just about everyone you know is carrying at least 1 car loan it is easy to buy into that idea. But the reality is that by organizing your income and expenses within a zero-based budget you can save enough money to pay cash for a car. Does it take self-discipline over time to achieve this? Yes, it does. But by organizing your money and making yourself (and your money) behave you can win.

Myth 2. You don’t earn enough money to avoid debt.

Winning with money is 20 percent math and 80 percent behavior. It’s not what you make, it’s what you spend. So begin with a zero-based budget and some determination to move your financial position forward and you would be surprised at the debt you can pay off.

Myth 3. You need a credit card for emergencies.

You don’t need a credit card for emergencies, you need an emergency fund. Debt sucks the life out of your finances and keeps you in a cycle of dependency. When you pay off all of your debt, you can build an emergency fund of actual cash so that when emergencies happen there is money in the bank to pay for it. This is all possible with you are in a debt-free position. Learn how to become debt free here. No gimmicks, just some commitment, and hard work.

Myth 4. You need a credit score

About the only reason you need a credit score is to borrow money. Since debt is a counterproductive way to lead your financial life why would you want to borrow money? And if you don’t borrow money, why do you need a credit score?

The people who sell you on the idea that you “need” a credit score and that you have to “build” your credit score are also the ones who loan you the money. Getting the picture?

You don’t need a credit score unless you want to borrow money. We think it is a better idea to kick debt out of your life and build an emergency fund so you don’t have to reach for credit cards anymore.

How to Get Out of Debt

Getting out of debt is like trying to lose weight. You can’t do it halfway and you can’t do it half-hearted either. Commitment is key and the best way to get out of debt is to put the peddle to the floor and go! You can wander into debt, but you can’t wander out. You have to be intentional and sometimes intense. The first step in getting out of debt is to quit using it. And that means you need an emergency fund.

Step # 1. Start organizing your money using a monthly zero-based budget.

If you are going to get out of debt, you’ll need to begin making your money do the right job. And this means building your monthly zero-based budget. Get a free zero-based budget pdf here. When you organize your money using a zero-based budget you are able to make sure that it is going where you need it to go. Compare this strategy to letting your money go where it wants to go when you have the urge for a fufu coffee drink. A budget is telling your money where to go instead of wondering where it went. Step 1 to getting out of debt is to begin using a monthly zero-based budget.

Step # 2. Save $1,000 as fast as you can for a starter emergency fund.

The average person using this plan saves $1,000 in less than 2 months.

Using your zero-based budget each month, assign a portion of your income to go toward your starter emergency fund of $1,000. Do this as fast as you can. Sell stuff if you have to. But save a thousand dollars as fast as you can so the next time you have an emergency, you don’t reach for the credit card. This is the beginning of your debt management plan. If you want to know how to pay off debt the first step is to quit using debt. And to kick things off let’s start with a thousand-dollar emergency fund.

Step #3. Debt Snowball. Line up all of your debts from smallest to largest.

The average person using this plan completes step two in 24 to 30 months.

Now, line up all of your debts from smallest to largest and begin by attacking the smallest balance first regardless of the interest rate. No doubt you’ll have some sophisticated well-meaning relative or friend that wants to argue math and interest rates. They’ll be quick to point out that if you pay off the debt with the lower interest rate first it will cost a bit more vs paying off the highest interest rate first. While we will admit their math is correct they are missing one key element to your predicament. Math didn’t get you into credit card debt, your behavior did. And no one has ever corrected behavior with math. So let’s stack up a win as soon as possible and use that momentum to carry us on to the next win. Keep that $1,000 emergency fund intact and start paying off your debts from smallest to largest. And by the way, to help you get more momentum, we recommend that you stop all investing during this step. You need all of your ammo focused on getting out of debt. Ready? Go! It’s game time.

Step #4. Save a Full Emergency Fund

Congratulations! You learned how to pay debt off! Now that you have kicked debt payments out of your life we are ready to make sure that we don’t end up there ever again. So we are going to save up a full emergency fund of 3 to 6 months of household expenses and set it aside in our savings account. So when life’s inevitable surprises occur, we have the money set aside to pay for them. When you have an emergency fund you mostly stop having emergencies. What we used to call emergencies are now more like an inconvenience. With a full emergency fund in place, you won’t need personal loans and you’ll soon find out that your credit score doesn’t matter anymore. No more need to make a balance transfer either.